Sector trends

Retail and leisure: a deeper dive into key subsectors

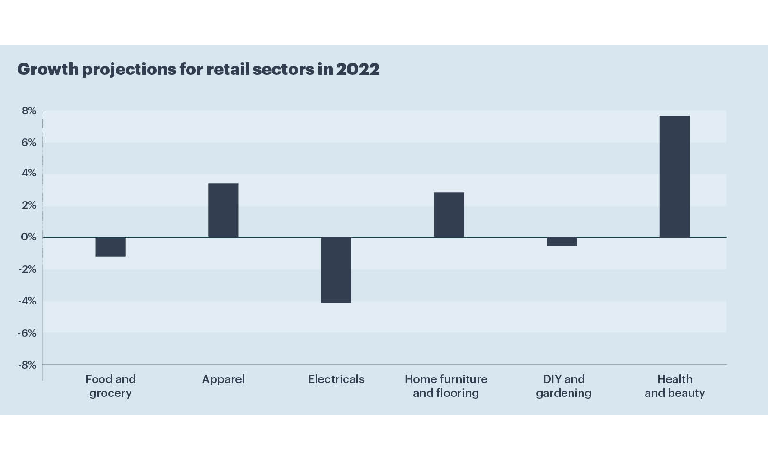

‘Top Retail and Leisure Trends for 2022’, published by Retail Economics and Ulster Bank, explores the industry’s prospects for the year against an unsettled economic backdrop. Here, we look at the main points affecting each subsector.

14 Mar 2022

. 4 min read

Economic pressures such as higher interest rates, rising inflation and increased National Insurance contributions spell an uncharted future for retail and leisure businesses in 2022.