Inflation is a measure of how much the prices of goods and services have risen over a particular period of time. This could be a snapshot of the big picture, such as a country’s overall increase of prices, or it can focus on certain goods or services such as food, energy or nursery fees. For example, if a loaf of bread costs £1.25 and then a year later £1.50, the rate of inflation for bread would be 20% for that year.

There are different measures, but the Office for National Statistics uses the Consumer Prices Index or CPI to track the overall figure talked about in relation to cost of living. The CPI records the monthly percentage change of each item in a typical ‘shopping basket’ of around 730 goods and services in comparison to the same time in the previous year. These goods are updated to reflect shopping trends.

The Bank of England (BoE), the UK’s central bank, has the job of ensuring prices don’t rise too quickly, so its primary objective, as set out in its mandate by the UK government, is to maintain price stability.

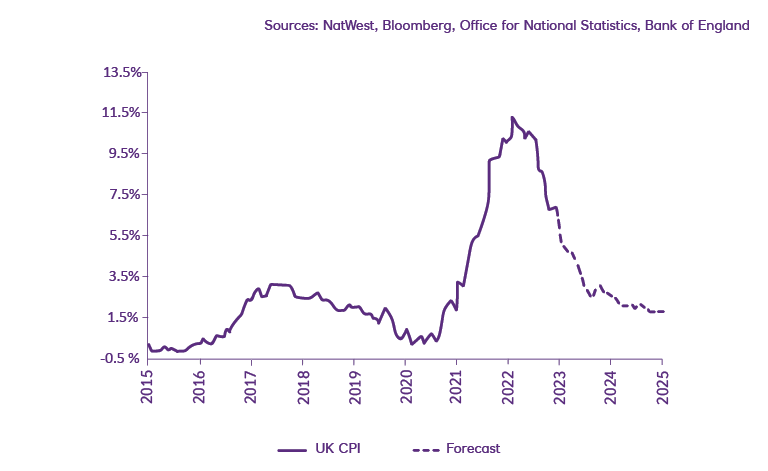

It has been given a yearly target inflation rate of 2% (an average of the prices in the shopping basket). This means that the Bank of England aims to keep inflation around this point, which is typically set at 2% for the CPI. The figure of 2% is calculated by taking an average of the prices in the shopping basket. At the present time inflation is 6.7% in the year to September 2023, the same rate as in August, but slightly down from July.