Economics

Monthly UK Economic Outlook: August

Our economists share their views on the key economic trends to watch in the month ahead.

05 Aug 2022

. 4 min read

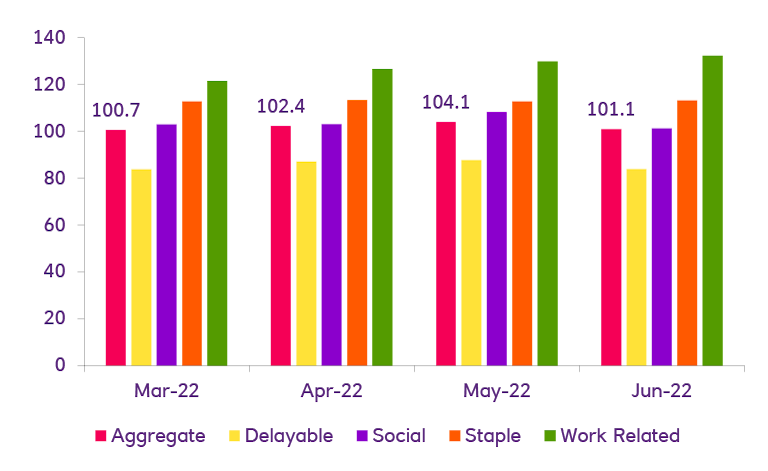

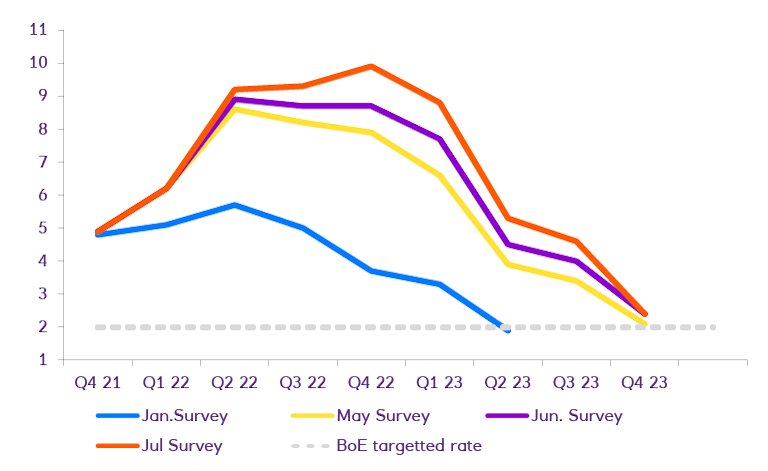

Economic conditions are worsening amid a squeeze in real incomes and tighter monetary policy – but there are signs of some respite on the horizon. For the moment, all eyes are on monetary policy. The Bank of England hiked the Bank Rate by 50 basis points at its meeting in August and signalled a tough economic environment through 2023. In the months ahead, it will have the unenviable task of trying to manage an increasingly delicate balance between growth and inflation.