Economics

Monthly UK Economic Outlook: April

Our economists share their views on the key economic trends to watch in the month ahead.

05 Apr 2023

. 4 min read

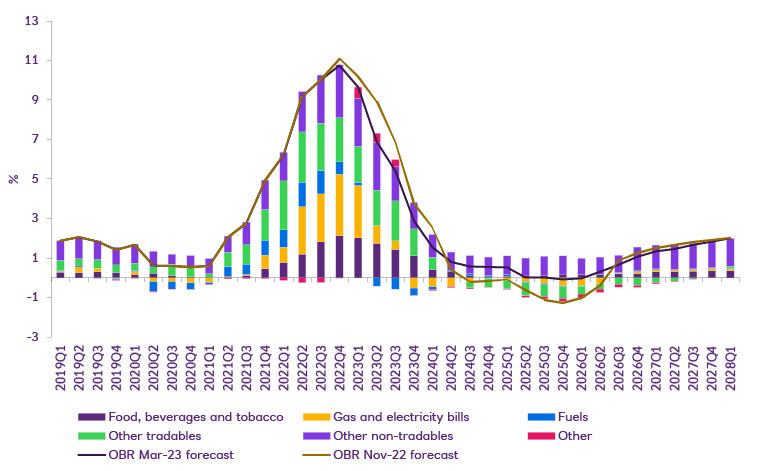

All in all, things are looking better than expected. The UK economy performed better than previously thought in Q4, and probably grew in Q1. GDP increased by 0.3% in January and healthy-looking business surveys for February and March point towards an improved near-term outlook. Consumer confidence is improving, too, reflected in a rise in spending. The decision to extend the Energy Price Guarantee will boost households’ disposable incomes and should result in inflation falling quicker in Q2.