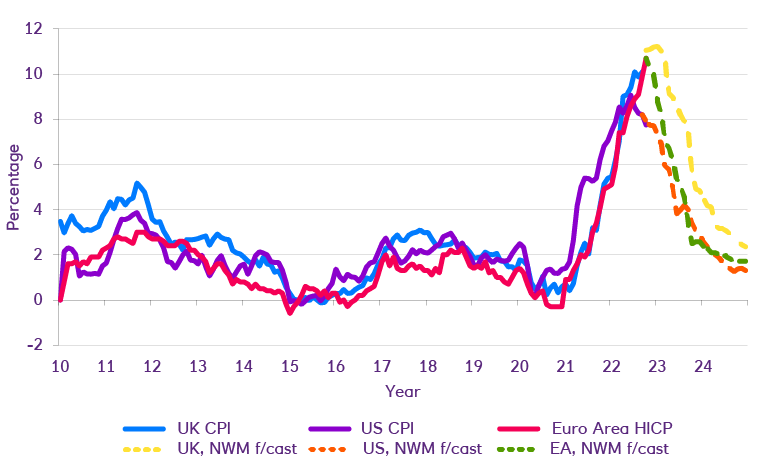

In 2023 we expect tension between the disinflationary effects of recession and the inflationary effects of lagging cost pressures working their way through the system and tight labour markets. Forward-looking indicators tend to emphasise disinflationary pressures, while lagging and current indicators retain a more inflationary feel.

A common feature of our US, eurozone and UK inflation outlooks is a degree of stickiness in core inflation in 2023 and 2024. Energy base effects will tend to reduce headline rates more rapidly than core measures, with the gap between the two narrowing sharply over the course of 2023.

The United States

We see subtly different factors at play in these regions. In the US, core CPI is expected to moderate from 6.3% at the end of 2022 to 3.2% by December 2023, and 2.1% by December 2024. The US dollar’s sustained strength is likely to weigh on core goods prices, while on the services side we expect prices to continue to increase (albeit less quickly than before) due to the shelter component.

The key factor likely to lead to sustained inflationary momentum in the US in 2023 is continued tightness in the labour market. In our view, for inflation to eventually get back toward 2% (the US Federal Reserve’s target), there needs to be a persistent situation in which there are fewer jobs than workers and somewhat fewer openings than unemployed workers. So far there has been no convincing evidence of wage pressures easing. Against a backdrop of a tight labour market, this will prevent core services inflation from slowing down significantly in 2023.

Eurozone

By contrast, wage pressures in the eurozone remain subdued. We view core inflation in this region less as a gauge of underlying inflation or a leading indicator and more a lagging reflection of energy prices. We expect some pick-up in wage inflation in the eurozone in the coming months, with the key question being whether this is one-off in nature or whether these pressures will persist.

The United Kingdom

In the UK, demand indicators are more subdued than in the US and total hours worked remain 0.6% below pre-pandemic levels. The UK has its own idiosyncrasies – notably a sharp increase in inactivity during and after the pandemic, including a near-400,000, 17.5% increase in those classified as long-term sick.

A key consideration is how permanent the reduction in UK labour supply is – the more permanent, the tighter the labour market and the higher that wage inflation would be expected to be. Conversely, to the extent that the move towards inactivity reverses in response to cost-of-living pressures and a turnaround in sickness trends, the higher the labour market slack in the UK.